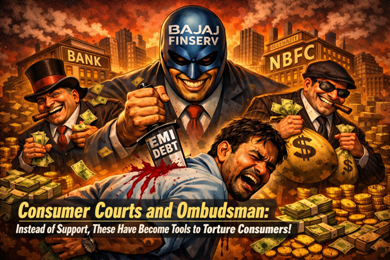

In India’s regulatory architecture, consumer forums and the RBI-backed Banking Ombudsman were envisioned as swift, accessible remedies for citizens facing exploitation by banks, NBFCs, and service providers. They were meant to reduce litigation, ensure accountability, and offer ordinary consumers a fair chance against powerful financial institutions. But for a growing number of complainants, these mechanisms now function less as shields for consumers and more as “safety valves” for corporate misconduct—absorbing public anger without delivering real justice.

What was designed as a grievance redress system is increasingly accused of becoming a procedural maze, keeping consumers entangled for years in paperwork, adjournments, and formalities. By the time a final order is passed—or not passed at all—many borrowers are financially and mentally exhausted, effectively deterred from approaching higher courts. The result: delayed justice that often resembles denied justice.

A recent case involving a borrower of a leading NBFC illustrates this troubling trend.

According to the complainant, after facing financial distress, he approached Bajaj Finance seeking a restructuring of his loan or a one-time settlement. His account, identified by him as Loan Account No. 401TPFFZ161475, had allegedly become difficult to service due to circumstances beyond his control. Instead of considering relief options, the company reportedly rejected both restructuring and settlement requests outright and continued to demand regular EMIs.

Left with no option, the borrower approached the RBI Ombudsman, expecting regulatory intervention. But the response, he claims, was merely procedural: he was asked to “wait for one month” while the company maintained its hardline stance. Even after repeated representations, no effective direction was issued to the NBFC to consider restructuring or settlement. The borrower alleges that the Ombudsman’s office, far from acting as a consumer protector, became a passive observer, allowing the company to continue its collection practices without accountability.

This is not an isolated complaint. Across the country, thousands of cases against banks and NBFCs are pending before consumer forums and ombudsman offices. Data from various legal trackers and court portals consistently show massive backlogs in district and state consumer commissions. While these bodies were supposed to provide “summary and speedy justice,” proceedings often stretch into years, during which interest accumulates, penalties mount, and borrowers sink deeper into debt.

Critics argue that this systemic delay serves a convenient purpose: it defuses public anger without threatening corporate power. The very existence of grievance mechanisms creates the appearance of accountability, but their functioning often protects institutions rather than consumers. In this sense, the system acts like a safety valve on a volcano—releasing pressure without addressing the forces that cause the eruption.

More troubling is the regulatory framework that allows NBFCs to charge exorbitant interest rates, often far above what traditional banks levy. While India calls itself a welfare state, regulatory by-laws and financial policies frequently favor lenders over borrowers. Consumer activists point out that weak enforcement, limited penalties, and slow adjudication create an environment where financial institutions can reject restructuring requests, continue aggressive recovery, and still remain legally insulated.

The complainant in this case goes further, alleging a deeper political economy behind the regulatory inertia. He claims that major financial corporations fund political parties through election donations, ensuring policy protection in return. Meanwhile, media houses—dependent on advertising from the same corporations—rarely highlight consumer grievances against powerful NBFCs and banks. The result is a silence that normalizes corporate impunity.

The question then arises: Where are the institutions meant to protect the public? Why does the government allow high-interest lending in a country grappling with unemployment, inflation, and debt distress? Why does the RBI Ombudsman, backed by statutory authority, appear reluctant to issue firm directions when companies refuse restructuring or settlement? And why are consumer forums, created as people-friendly courts, overwhelmed to the point of ineffectiveness?

The Supreme Court and higher judiciary have, on several occasions, emphasized that access to justice must be meaningful, not merely procedural. Yet on the ground, consumers continue to experience what they describe as harassment through delay, technicalities, and institutional indifference.

This case, like thousands of others pending across forums and ombudsman offices, is a warning. It reveals how grievance redressal mechanisms can be transformed from instruments of justice into buffers that protect corporate interests while exhausting ordinary citizens.

If consumer forums and the ombudsman system continue to function as procedural formalities rather than decisive regulators, their very purpose will stand defeated. In a democracy that claims to be welfare-oriented, regulatory bodies must act not as neutral spectators but as active defenders of consumer rights. Otherwise, the promise of justice will remain trapped in files—while the burden of debt, delay, and despair continues to fall on those least able to bear it.

Leave a Reply